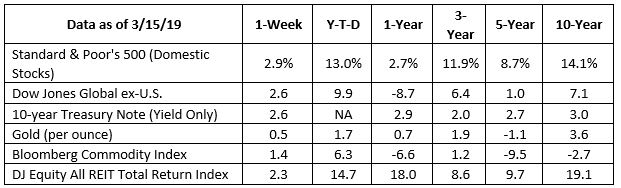

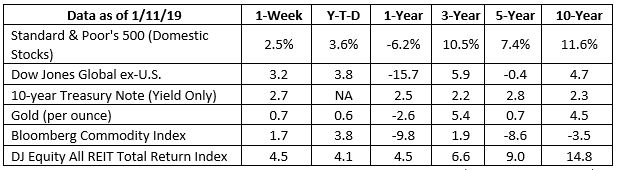

At dinner this past week with a long-time client, I was asked what I thought of Jim Cramer. I kindly said, “He’s a great speaker, entertainer, and educator, but I’m not sure of his investment advice track record, let me dig up the facts for you.” An Examination of a...

Digital Assets and Baby Boomers

How many password-protected accounts do you have?

Whether you keep them locked in the depths of your memory, use a password manager, or have a written record of your passwords (which is certainly not recommended), take a quick count. You are most likely to find you have some or all of these types of accounts:

- Email accounts

- Social media accounts

- Online storage accounts

- A domain name

- Online bank accounts

- Online brokerage accounts

- A website or blog

- Online shopping accounts

- Online bill paying

- Photo and video sharing accounts

- Gaming accounts

- Materials and coding that are copyrighted

These are all digital assets. They are part of your virtual life, as is any digital property you own, such as computers, external drives, storage devices, smart phones, digital cameras, e-readers, and other devices.

Digital assets should be part of your estate plan

Unless you live off the grid, it’s likely your digital life will outlive you and become a part of your legacy. Your digital assets may have significant financial or personal value for your heirs. Consequently, you should give some thought to how these assets should be managed after your death.1

The catch is digital estate planning can be tricky. Many digital accounts and assets cannot be transferred to a new owner because they are not your property. Assets that fall into this category are subject to contracts and licensing agreements established with a service provider.1

For example, if you’ve spent significant sums accumulating a virtual music library, you may not be able to pass it on through a will or another estate planning tool because you do not own the digital music files, according to Nolo.com. This may also be true with other types of accounts.1

“Social network accounts, domain name registrations, email accounts, and most other types of online accounts are ‘yours’ by license only. When you die, the contract is over and the business that administers the account controls what happens to it,” explained Betsy Simmons Hannibal on Nolo.com.1

This doesn’t mean you have no control over what happens to these accounts. Your estate can leave instructions about account management and should provide a complete record for your executor. Jeffrey Salas offered an opinion about best practices on LegalZoom.com. He recommended:2

- Checking the account providers’ Terms of Service/Terms of Use. Work with your estate planning attorney and the digital executor you’ve appointed to review requirements for different types of accounts. For example:

- Leave usernames and passwords for any online financial accounts – banking, utilities, brokerage, mortgage, retirement plan, life insurance, tax preparation, or others – to the executor as they will need this information to pay bills, close accounts, and administer your estate.1

- Social media companies have diverse policies regarding the management of digital assets upon the death of the user. Some delete or deactivate accounts after being notified of a death. Others put accounts into ‘memorial’ status.1

- In general, companies will not know about the death until they’re notified. As a result, a digital executor who is armed with passwords may be able to access your account to post final updates, delete items (per estate instructions), or delete/deactivate accounts.1

- Email accounts, online communities, and blog management may also be guided by provider agreements. However, your executor may be allowed to notify friends or followers of your death and then delete, print, or archive your communications.1

- Digital photos that are stored online may be passed on through a will or another estate planning tool.1

- If you have one or more websites, domain names may have value and they may be transferrable.1

- If you have an online store, you may want to leave instructions about what should happen to the store, the items for sale, and any income or profits that may continue to arrive.

2. Add language regarding digital assets to your will and/or trust. Currently, there is no uniform federal law to guide the management of digital assets.2 At the start of 2017, Kiplinger reported, “Federal law regulating access to digital property does not yet exist. At this time, 29 states have established legislation or laws to protect digital assets and to provide a deceased person’s family procedures and rights to manage those accounts and assets after death.”3 Regardless, it can still be a good idea to include language that specifies your wishes for the treatment of each of your digital accounts.2

3. Check the law in your state. Talk with your attorney or advisor about whether any laws your state has that apply to digital assets, and make sure your estate plan is consistent with these laws.2

While estate and inheritance laws are behind the curve when it comes to digital assets, it is important to inventory your digital assets and decide how they should be managed upon your death. If you would like additional information about estate planning, please give us a call.

Sources:

1 https://www.nolo.com/legal-encyclopedia/a-plan-your-digital-legacy.html

2 https://www.legalzoom.com/articles/what-happens-to-your-digital-assets-when-you-die

3 https://www.kiplinger.com/article/retirement/T021-C032-S014-put-digital-assets-in-your-estate-plan.html