The Big Guys Move InOn September 13, 2022, the biggest of the big guys on Wall Street came out with a rather earth-shaking announcement. None other than Fidelity, Citadel Securities, and Charles Schwab have launched a new cryptocurrency exchange. In the words of the...

Market Commentary – March 18, 2019

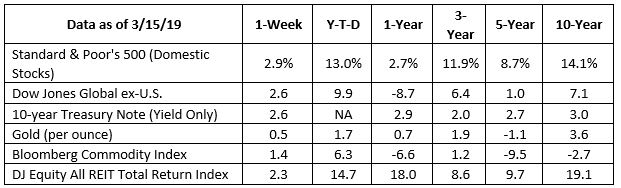

Stock and bond markets rallied.

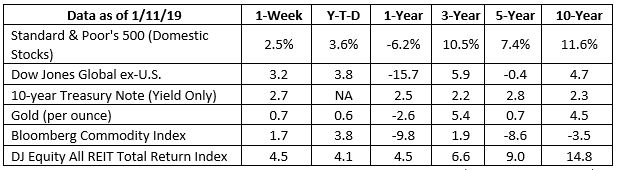

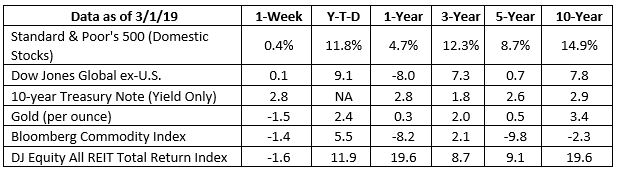

Last week, major U.S. stock indices finished higher for the 10th time in 12 weeks. Bond markets moved higher, too, with the yield on 10-year Treasuries dropping just below 2.6 percent, reported Randall Forsyth of Barron’s. Yields on 10-year Treasuries haven’t been this low since January 2018.

The simultaneous rallies are curious because improving share prices are often an indication of a strong or strengthening economy. Improving bond prices tend to be a sign of weakening economic growth, reported Michael Santoli of CNBC.

Why are U.S. stock and bond markets telling different stories?

It may have something to do with investor uncertainty. A lot of important issues remain unsettled. The British government appears incapable of resolving Brexit issues, the United States and China have not yet reached a trade agreement, and recent economic reports have caused investors to take a hard look at the U.S. economy.

Barron’s pointed out investors appear to be hedging their bets by favoring in utilities and other stocks that have bond-like characteristics and participate in the stock market’s gains. An investment strategist cited by Barron’s explained: “The strength in utilities reflects the attitude of investors who ‘don’t really buy the rally’…While they’re skittish, they still want to participate in the stock market rally but opt for its most conservative sector.”

We’ve seen this before with stocks and bonds, according to a financial strategist cited by Patti Domm of CNBC. “It’s a little bit of a funky correlation. We’ve had both things rallying, which is strange. This is what happened in 2017, when all asset classes did well. In 2018, nothing did well…I would suspect it goes away soon.”

Times like these illustrate the importance of having a well-diversified portfolio.

Gen Xers and millennials: what are your priorities? The 2018 Insights on Wealth and Worth survey provided some startling information about the priorities of high net worth (HNW) investors. More than one-half (54 percent) indicated long-term capital appreciation was a higher priority than income generation. The other 46 percent were looking for steady income.

Let’s look at the percentages by age group:

- Millennials: 56 percent capital appreciation / 44 percent steady income

- Gen X: 56 percent capital appreciation / 44 percent steady income

- Baby Boomers: 56 percent capital appreciation / 44 percent steady income

- Silent Generation: 46 percent capital appreciation / 54 percent steady income

Millennials (ages 21 to 37), Gen Xers (ages 38 to 53), and Baby Boomers (ages 54 to 72) prioritize steady long-term income to the same extent.

Older investors, who are near or are in retirement, tend to emphasize steady long-term income because they need to maintain their standard of living in retirement. However, one of the advantages of youth is these investors have the time and flexibility to take on higher levels of risk and recover from any market downturns. In other words, younger investors prioritize capital appreciation (i.e., growth) while older investors prioritize income.

It’s important for younger investors to consider their life goals and how their finances may support the pursuit of those goals.

Weekly Focus – Think About It

“There are risks and costs to action. But they are far less than the long range risks of comfortable inaction.”

–John F. Kennedy, 35th President of the United States

Best regards,

John F. Reutemann, Jr., CLU, CFP®

P.S. Please feel free to forward this commentary to family, friends, or colleagues. If you would like us to add them to the list, please reply to this email with their email address and we will ask for their permission to be added.

Investment advice offered through Research Financial Strategies, a registered investment advisor.

S&P 500, Dow Jones Global ex-US, Gold, Bloomberg Commodity Index returns exclude reinvested dividends (gold does not pay a dividend) and the three-, five-, and 10-year returns are annualized; the DJ Equity All REIT Total Return Index does include reinvested dividends and the three-, five-, and 10-year returns are annualized; and the 10-year Treasury Note is simply the yield at the close of the day on each of the historical time periods.

Sources: Yahoo! Finance, Barron’s, djindexes.com, London Bullion Market Association.

Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. N/A means not applicable.

Most Popular Financial Stories

Bitcoin – There’s No There There

read more

Special Message

Look! Have You Noticed? Listen to any politician or any news commentator these days, and they always begin a discussion or answer a question like this: Look, when I served in the Senate …. Look, as I wrote in my last column …. Look, if the Republicans won’t …. Look,...

Special Market Update

Inflation is proving to be far more tenacious than financial markets had hoped.The idea that inflation peaked in March was put to rest last week when the Consumer Price Index (CPI) showed that inflation accelerated in May. Overall, prices were up 8.6...

Special Update

All,You undoubtedly have heard reports that the world’s supply of wheat and corn are in jeopardy due to Ukraine and Russia both missing this season’s planting window for obvious reasons (click the link above to read more details). Did you know that Russia...

Significant Shrinkage

Significant Shrinkage Buffeted by Inflation Is it time to double check your household budget? Chances are the budgeted expenditures of the vast majority of Americans are about to get buffeted. Or so says the Oracle of Omaha. In the latest shareholder...

How to Manage Your Money and Your Risk Exposure

This is an excellent example of one of our more popular client webinars where we detail what is happening in the market, what makes us so successful and different from other advisors, and how it effects our clients' portfolios.

* Government bonds and Treasury Bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

* Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate and credit risk as well as additional risks based on the quality of issuer coupon rate, price, yield, maturity, and redemption features.

* The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. You cannot invest directly in this index.

* All indexes referenced are unmanaged. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

* The Dow Jones Global ex-U.S. Index covers approximately 95% of the market capitalization of the 45 developed and emerging countries included in the Index.

* The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

* Gold represents the afternoon gold price as reported by the London Bullion Market Association. The gold price is set twice daily by the London Gold Fixing Company at 10:30 and 15:00 and is expressed in U.S. dollars per fine troy ounce.

* The Bloomberg Commodity Index is designed to be a highly liquid and diversified benchmark for the commodity futures market. The Index is composed of futures contracts on 19 physical commodities and was launched on July 14, 1998.

* The DJ Equity All REIT Total Return Index measures the total return performance of the equity subcategory of the Real Estate Investment Trust (REIT) industry as calculated by Dow Jones.

* The Dow Jones Industrial Average (DJIA), commonly known as “The Dow,” is an index representing 30 stock of companies maintained and reviewed by the editors of The Wall Street Journal.

* The NASDAQ Composite is an unmanaged index of securities traded on the NASDAQ system.

* International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

* Yahoo! Finance is the source for any reference to the performance of an index between two specific periods.

* Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

* Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

* Past performance does not guarantee future results. Investing involves risk, including loss of principal.

* You cannot invest directly in an index.

* Stock investing involves risk including loss of principal.

* The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee it is accurate or complete.

* There is no guarantee a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

* Asset allocation does not ensure a profit or protect against a loss.

* Consult your financial professional before making any investment decision.

* To unsubscribe from the Weekly Market Commentary please reply to this e-mail with “Unsubscribe” in the subject.

Sources:

https://www.barrons.com/articles/why-investors-are-rushing-into-stocks-that-act-like-bonds-51552700368?mod=hp_DAY_4

https://www.cnbc.com/2019/03/14/stock-investors-wonder-whether-the-bond-market-knows-something-they-dont.html

https://www.bls.gov/news.release/empsit.nr0.htm

https://www.barrons.com/articles/why-utility-stocks-are-worth-a-second-look-1531344310

https://www.cnbc.com/2019/02/06/bonds-and-stocks-going-up-together-could-be-signaling-market-at-an-inflection-point.html

https://ustrustaem.fs.ml.com/content/dam/ust/articles/pdf/insights-on-wealth-and-worth-2018/Detailed_Findings.pdf (Pages 3 and 39)

https://www.moneyunder30.com/asset-allocation-for-investors-under-thirty

https://www.brainyquote.com/quotes/john_f_kennedy_109216?src=t_risks