Look!

Have You Noticed?

Listen to any politician or any news commentator these days, and they always begin a discussion or answer a question like this:

Look, when I served in the Senate ….

Look, as I wrote in my last column ….

Look, if the Republicans won’t ….

Look, if the Democrats won’t ….

Just listen to the evening news tonight, and you’ll see what I mean. They all say “Look!”

Drives me a bit nuts.

But Maybe …

But maybe we should “look.” Look around us. Look at some statistics. Look at some developing trends. And when we do look, what do we see?

Economic Destruction

It’s not a pretty sight. Inflation drives millions to seek second jobs. Rapidly increasing mortgage rates are destroying the housing market. Applications for refinancing (to pay for higher prices of everything) have plummeted. Big retail outlets must rid themselves of bloated inventories, at a huge cost to their bottom lines. Truncated summer vacations might lower household expenditures for gasoline, but they also help shrink economic activity and add to recession fears. And if that’s not enough, a six-van tour service in Hawaii now needs only one of those vans―pain in paradise. It’s not a pretty sight.

How Bad Is It?

Seeking Second Jobs

Look at employment trends. If you’ve gone to any restaurant or driven up to a McDonald’s, surely you’ve seen the plethora of Help Wanted signs. And if you’ve gone into some of those restaurants, you often see lines waiting for a table but a bunch of empty tables inside. The owners can’t get enough wait staff or cooks to serve a capacity crowd.

Where did everybody go? Many sat out Covid and cashed Covid checks supplemented with unemployment insurance. They liked living at home or in their parents’ basements and just didn’t return to the workforce.

That’s about to change. In the words of Columbia Business School professor Mark Cohen:

At the end of the day, there are only so many credit cards you can load up and things you can avoid spending on before you come to the reality that maybe you have to pick up a second job. It’s about how much do you bring in every month, how much do you spend—if you’re in a deficit position, you have to find another job or an additional job.[i]

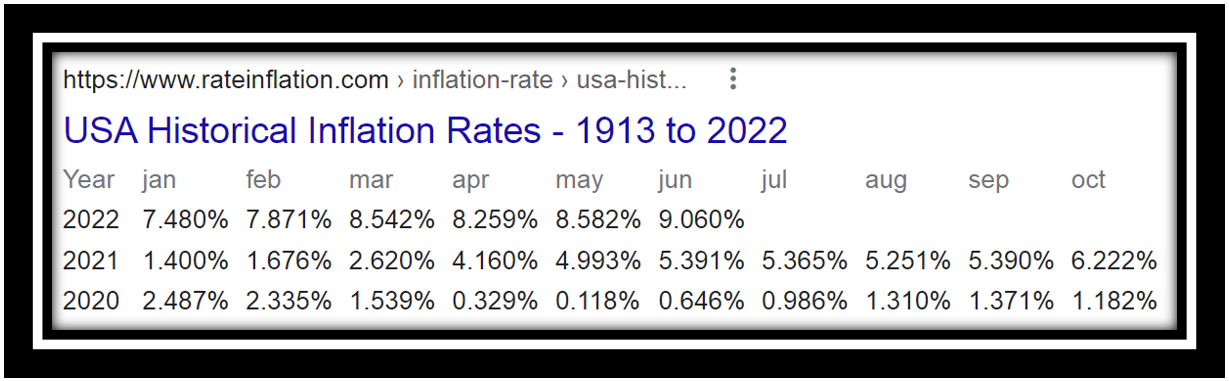

The inflation that used to be “transitory” has now transmogrified into an inflation that is “rampant.” Just two years ago, inflation hovered around 2.0%. Now in June 2022, it’s jumped above 9%. Not a pretty sight:[ii]

These elevated inflation rates are driving millions of Americans to seek a second job. Many of these second jobs are “full-time jobs,” which the Bureau of Labor Statistics (BLS) defines as a job requiring at least 35 hours per week. Thousands of our fellow citizens are forced to work two full-time jobs, or 70 hours each week:

426,000 Americans worked that much in June, compared to 308,000 in February 2020, according to the St. Louis Federal Reserve Bank’s analysis of BLS data.[i]

The numbers grow exponentially when we look at the number of Americans seeking second part-time jobs.

A new survey from Bankrate.com shows that, because of inflation, 41% of Americans say they need to pick up a second job in order to make ends meet. That’s up from 31% in 2019.[ii]

What? Forty-one percent of Americans. How many tens of millions of people is that? Not a pretty sight.

Housing Market

Look at what’s happening in the housing market―often a barometer of the economy at large. What was a boom for home-sellers has become an exercise in price-slashing:

The pandemic housing boom is careening to a halt as the fastest-rising mortgage rates in at least half a century upend affordability for homebuyers, catching many sellers wrong-footed with prices that are too high. It’s an astonishing turnaround. Just a few months ago, house hunters felt pushed to make offers within days, waive inspections and bid way above asking. Now they can sleep on it and maybe even shop for a better deal.[iii]

The post-pandemic high home prices of just a few months ago are now driving buyers away. So sellers must dramatically reduce their prices:

The turn in the US housing market has been sharp and swift. Just ask Karlyn and Jack Stenhjem, would-be downsizers who dropped the asking price for their home near Seattle by almost $100,000 since May.

[Their] house, with private access to lakes and trails, is now available for $899,000, a price that makes Karlyn Stenhjem “cringe.”[iv]

ReFi Market―Up 4%?

Look at the refinance market. When inflation eats into disposable income, people seek other sources of cash. Many were tapping into their home equity by refinancing their mortgages at progressively lower rates. Not now. Those mortgage rates are going through the roof (so to speak). But a week or so ago, we saw refinance demand increase by 4%. But guess what ….:

Refinance demand rose 4% for the week but was 76% lower than the same week one year ago.[v]

No, down 76%. So another source of extra cash bites the dust:

Total mortgage application volume was 52.7% lower last week than the same week one year ago, according to the Mortgage Bankers Association’s seasonally adjusted index. Sharply rising interest rates are decimating refinance volume, and those rates, along with sky-high home prices and a shortage of houses for sale, are hitting demand from potential buyers.[vi]

Unloading Retail Inventories

Look at what the biggies are doing. Target, WalMart, and other retail giants had it all figured out: When the pandemic ended, there would be huge pent-up demand. The shut-in consumers would spread their wings and open their purses and wallets. The payday would be huge

Oops. The heavy hand of inflation said no to those plans. Consumers certainly felt the new-found freedom of escaping the harsh Covid lockdowns, but inflation prevented them from buying high-end retail items and expensive clothing. Instead, they spent their money on gasoline, food, and other necessities.

The retailers faced a gigantic dilemma: What to do with bloated inventories? Put them on-sale? Offer a BOGO (Buy One Get One Free)? Store the goods for better times ahead? Offload them to bargain sellers like TJ Maxx?

Reuters wrote an interesting article about this quagmire: Sell, Stow or Dump? Retailers Wrestle with Mountain of Unsold Stock:

In the United States, clothing sales fell 89% in April from the same month in 2019, while in Britain clothing sales sank by 50% compared with an already-squeezed March.[vii]

So the anticipated post-Covid demand just isn’t there. If the big retailers opt to off-load expensive brands, savvy consumers should stand ready to cop some fabulous deals. Look at the plans of one California socialite:

“We’re going to see the most insane sales,” said Melissa McAvoy, founder of events company Luxury Experience & Co, who lives in the celebrity-studded Los Angeles suburb of Calabasas.

The 43-year-old said she planned to snap up merchandise at a discount, to then resell it at a higher price online at a site such as California-based Poshmark, which also makes money by taking a commission on sales.

“I’m going to get a tonne of stuff and either wear it once or put it on Poshmark,” she said.[viii]

Truncated Vacations

Look, or in this case, listen to identical conversations―typically between a Mom or Dad and their teenaged children―echoing throughout households across the country:

Mom or Dad: “But we are going to the beach this summer …. Just not quite as long.”

Teenaged Son or Daughter: “Quite? Last year we went for three weeks. And this year just one? That’s not fair.”

In millions of household budgets, money ordinarily set aside for vacations has jumped over into the column named “Gasoline” or “Weekly Food Budget.” Stats bear this out:

Majorities say they are likely to take fewer leisure trips (57%) and shorter trips (54%) due to current gas prices, while 44% are likely to postpone trips, and 33% are likely to cancel with no plans to reschedule. 82% say gas prices will have at least some impact on their travel destinations.[ix]

Needless to say, fewer people on the road affects the local economies of countless communities.

One short story from paradise makes the point:

Sunsets, surf and sand are still draws for visitors to Hawaii, but new statistics show their numbers are lower than usual for this time of year. That’s a big concern for those in the tourism industry, such as Carey Johnson, who runs Custom Island Tours. “We have four tour vans, I have six drivers,” she said. “So we can possibly be doing four tours a day, but right now we’re averaging less than one tour a day.”[x]

Look! Look Around You

You don’t have to look far to realize that this country―indeed, the entire globe―faces some dire economic circumstances. After the first quarter’s 1.6 percent decline in GDP and the second quarter’s 0.9 percent decline,[xi] the country officially entered a recession, according to traditional economic theory (two consecutive quarters of negative economic growth).

The White House begs to differ:

What is a recession? While some maintain that two consecutive quarters of falling real GDP constitute a recession, that is neither the official definition nor the way economists evaluate the state of the business cycle. Instead, both official determinations of recessions and economists’ assessment of economic activity are based on a holistic look at the data—including the labor market, consumer and business spending, industrial production, and incomes. Based on these data, it is unlikely that the decline in GDP in the first quarter of this year—even if followed by another GDP decline in the second quarter—indicates a recession.[xii]

Look, whether a recession begins with two consecutive quarters of negative growth or some other definition prevails, our citizens know that today’s economy isn’t doing the heavy lifting needed to sustain the livelihoods of 332,403,650 Americans alive on January 1 of this year.[xiii]

Will we come out of this mess? Yes, Americans always do. When? No one knows. But we can all look around us and see that things probably won’t get better before they get a whole lot worse.

But better they will get.

One day.

Call US

As always, please call us at 301-294-7500. We are happy to answer any questions you have.