Financial security and peace of mind in retirement doesn’t just happen ….

It takes proper long-term planning, commitment, and yes, money.

1. Save, Save and Save! And Stick to Your Goals

If you are already saving, whether for retirement or another goal, keep going! You know that saving is a rewarding habit. If you’re not saving, it’s time to get started. Start small if you have to and try to increase the amount you save each month. The sooner you start saving, the more time your money has to grow (see the chart below). Make saving for retirement a priority. Devise a plan, stick to it, and set goals. Remember, it’s never too early or too late to start saving.

2. Know Your Retirement Needs

Retirement is expensive. There is a long-held estimate that you’ll need about 70 percent of your pre-retirement income—lower earners, 90 percent or more—to maintain your standard of living when you stop working.

Take charge of your financial future. The key to a secure retirement is to plan ahead.

3. Contribute to Your Employer’s Retirement Savings Plan

If your employer offers a retirement savings plan, such as a 401K plan, sign up and contribute all you can. Your taxes potentially will be lower, your company may kick in more, and automatic payroll deductions make it easy for you to contribute.

Over time, compound interest and tax deferrals make a big difference in the amount you will accumulate.

Find out about your plan. For example, how much would you need to contribute to get the full employer contribution (401K match) and how long would you need to stay in the plan to get that money (401K vested).

4. Learn about Your Employer’s Pension or Plan

If your employer has a traditional pension plan, check to see if you are covered by the plan and understand how it works. Ask for an individual benefit statement to see what your benefit is worth. Before you change jobs, find out what will happen to your pension benefit. Learn what benefits you may have from a previous employer. Find out if you will be entitled to benefits from your spouse’s plan.

More information is available by reading the U.S. Department of Labor’s publication about protecting your pension: What You Should Know About Your Retirement Plan. (See the reference on page 2 of this article.)

We Can Help With Your 401K!

So, should you invest in your employer’s 401K account if you’re confused and looking for help with your retirement? Consulting with a professional investment advisor at Research Financial Strategies to help make important decisions with your 401K not only creates less fear of the unknown but we will help guide you to a more successful retirement. Research Financial Strategies offers ongoing management (401K advisor) of your employer 401K. Our years of experience will help navigate your 401K toward your goals.

read more: 401K Second Opinion, How To Rollover A 401K

Changing your investment mix to the stronger performers will benefit you in the long run.

5. Consider Basic Investment Principles

How you save can be as important as how much you save. Inflation and the types of investments you make play important roles in how much you’ll have saved at retirement. Know how your savings or pension plan is invested. Learn about your plan’s investment options and ask questions.

Put your savings in different types of investments. For example, although it may make you appear to be loyal to your employer, investing all of your 401K assets into solely your company stock is far from the best investment decision. By diversifying, you are more likely to reduce risk and improve return. Your investment mix may change over time depending on a number of factors such as your age, goals, and financial circumstances. Plus, if an investment is performing sub-par, its might be time to move your funds to a better performing choice. Financial security and knowledge go hand in hand.

6. Don’t Touch Your Retirement Savings

If you withdraw your retirement savings now, you’ll lose principal and interest, and you may lose tax benefits or have to pay withdrawal penalties. If you change jobs, leave your savings invested in your current retirement plan, or roll over to an IRA or your new employer’s plan.

7. Ask Your Employer to Start a Plan

If your employer doesn’t offer a retirement plan, suggest that it start one. There are a number of retirement savings plan options available. Your employer may be able to set up a simplified plan that can help both you and your employer.

Research Financial Strategies offers 401K solutions for businesses of all sizes. Whether its a new 401K plan or just in need of better management and support, we are here to help.

8. Put Your Money into an Individual Retirement Account - IRA

The individual retirement account (IRA) was created decades ago as defined benefit pension plans were declining. Becoming more popular as workers started to take control of their own retirement savings, the IRA offers individuals an opportunity to save for retirement in a tax-advantaged account.

The traditional IRA and Roth IRA accounts are the most popular types of IRAs.

You can also start your own IRA with almost any amount of money up to the yearly maximum contribution limits. IRAs may also provide tax advantages by potentially lowering your net taxable income.

When you open an IRA, you have two options—a Traditional IRA or a Roth IRA. The tax treatment of your contributions and withdrawals will depend on which option you select. Also, the after-tax value of your withdrawal will depend on inflation and the type of IRA you choose. IRAs can provide an easy way to save. (You can set it up so that an amount is automatically deducted from your checking or savings account and deposited in the IRA.)

Find out more information about IRAs: Traditional IRA vs Roth IRA

Visit the Internal Revenue Service’s website to see current allowable yearly contribution limits for IRAs.

9. Find out about Your Social Security Benefits

Social Security pays benefits that are on average equal to about 40 percent of what you earned before retirement.

You may be able to estimate your benefit by using the retirement estimator on the Social Security Administration’s website. click here

10. Ask Questions

While these tips are meant to point you in the right direction, you’ll need more information. read more: Social Security Benefits

Talk to your employer, your bank, your union, or contact us to speak with one of our financial advisors.

Ask questions and make sure you understand the answers. Get practical advice and act now.

Quick Facts

FACT 1: Fewer than half of Americans have calculated how much they need to save for retirement.

FACT 2: In 2012, 30 percent of those who had 401K coverage available didn’t participate.

FACT 3: The average American spends 20 years in retirement.

Putting money away for retirement is a habit we can all live with. read more on Saving For retirement

Remember … saving matters!

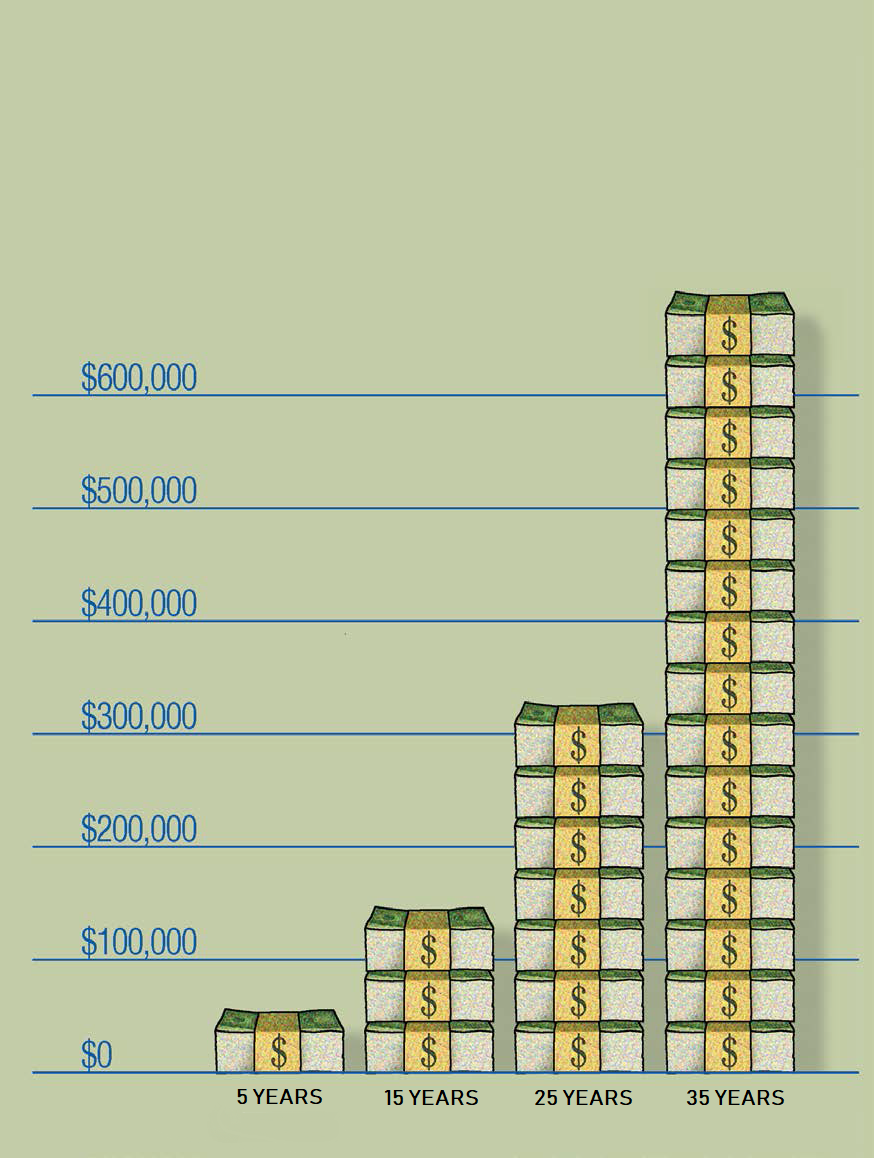

The Advantage of Starting Early

Start saving for your retirement now! This chart shows what you could potentially accumulate after 5, 15, 25, and 35 years if you saved $5,000 each year, and your money earned 7% annually.*

Generally, the earlier you start saving the more time you have to invest and the earlier you start the more time your savings have to grow. And thanks to compound interest, the money you would have otherwise paid toward income tax remains in your account to earn even more money.

*This information is hypothetical and is provided for informational purposes only. It is not intended to represent any

specific return, yield, or investment, nor is it indicative of future results.

When you’re choosing a Wealth Manager, you need to be sure they’ll listen to your requirements and support you in achieving your objectives. With Research Financial Strategies, you can be confident that together, we will develop a relationship on your terms.

– Jack Reutemann, CEO & Founder

Recent Market News

Weekly Market Insights | Markets Hold Broad-Based Rally

Stocks staged a broad-based rally last week on investors’ hopes for a lasting Middle East ceasefire, hitting fresh record highs along the way. The Standard & Poor’s 500 Index rose 3.44 percent, while the Nasdaq Composite Index added 4.25 percent. The Dow Jones...

Investment Ponderings from Jack Reutemann

At dinner this past week with a long-time client, I was asked what I thought of Jim Cramer. I kindly said, “He’s a great speaker, entertainer, and educator, but I’m not sure of his investment advice track record, let me dig up the facts for you.” An Examination of a...

Weekly Market Insights | Market Attention Turns to Trade and Oil

Stocks fell last week as an up-and-down mix of trade progress and anxiety, economic news, and geopolitical tensions netted out. The Standard & Poor’s 500 Index slid 0.39 percent, while the Nasdaq Composite Index slipped 0.63 percent. The Dow Jones Industrial...

Need A Consultant?

Our focus is on your life and priorities. Not just your portfolio. That’s why we start by listening and learning about you. Each individual client has different needs and concerns that need to be addressed. And because we carefully listening to those concerns, we will gain important information that will help us to best serve our clients and help protect their financial futures.