10 of the Most Common Employee 401K Questions, Answered

When you think about investing in the long term, don’t just stock up on bulk stacks of printer paper and buy out all the peanut butter at Costco. While it’s important to plan for things like your future needs and time savings (hey, that printer paper is gonna last a while), few things are more important than ensuring long-lasting and dependable financial resources to support you late into life.

Instill the importance of long-term investing to your employees by helping answer their questions about 401K retirement plans. Right now, they’re likely groaning at the thought of setting one up, deciding how much to put aside, transferring their account over if they need to change companies, and so on. It’s a world chock-full of jargon, and we’re here to break it all down for you.

1. What is a 401K plan, and why is it called that?

A 401K is a retirement plan: cash taken out of your current payroll that will replace employment income when you’re ready to enter the next stage of your life. If you elect to contribute to your plan, the percent you choose will be automatically deducted from your paycheck each pay period. This money is taken out before your paycheck is taxed (so more of it can go to your retirement instead of the government). The contributions are invested at your discretion into one or more funds provided in the plan. While the investments grow in your 401K account, you still don’t pay any taxes on it. Nice!

Oh yeah, and it’s named for the section of the tax code that governs it (we know, so clever).

2. What’s my company’s role in my 401K?

You’ll often hear about employer-sponsored plans, which is when your company takes responsibility for establishing and maintaining employees’ 401K plans. Employers often “match” employee contributions, meaning they’ll agree to contribute a set percent of money to your plan if you also contribute a certain percent.

Say your company has a 50 percent match policy, and you decide to contribute six percent of your annual salary to your 401K. Your company would then contribute three percent, and your total contributions for the year would be nine percent of your annual salary.

You should always maximize your employer’s match — it’s basically free money, and it’s also safe from taxation while it’s sitting in a 401K account.

3. Do all companies match 401K contributions?

Though it’s common practice at larger companies, employers are not required to match contributions. A company has complete control over whether or not they do, since the match is a form of profit sharing. If your employer is not highly profitable or going through a tight financial situation, they may opt not to match the contributions. Whether or not your company offers a match, though, shouldn’t deter you from regularly adding money to your own 401K.

4. Are all 401K plans created equal?

Not quite. Having these qualities can make a plan more advantageous than others:

- Ability to participate right away: Many companies require one to three months (or even up to a year!) of employment before workers qualify to join the retirement plan. The sooner you can participate and start taking advantage of any employer match, the better.

- A generous 401K match: Meaning the more you contribute, the more your employer will, too. That’s just more money in your (retirement) pocket.

- Immediate vesting: You won’t get to keep your employer’s contributions to your 401K account until you are vested in the plan — and some companies require more time in service before you can keep the entire match provided.

- Low expenses or the plan sponsor pays most fees: There are fees associated with establishing and maintaining 401K accounts. It’s great if you can hook up with an employer who is generous enough to cover (fully, or a good margin of) these fees.

- Automation: Automatic enrollment, deductions, and filing will make your life so much easier. Need we say more?

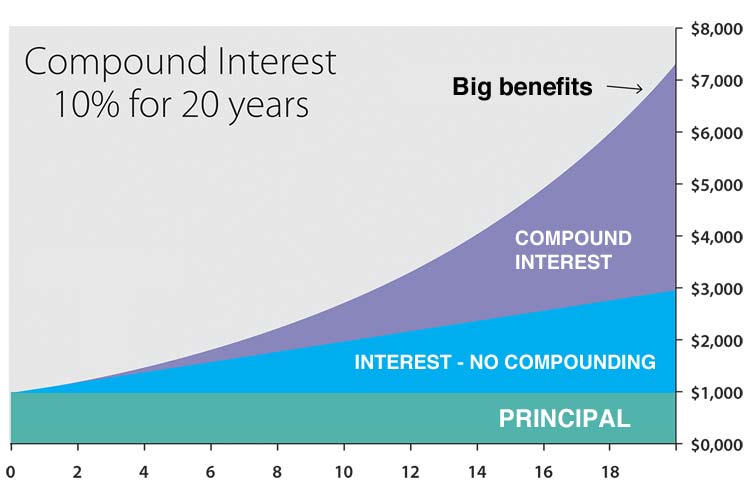

5. When do I need to start contributing?

The most important thing to know about 401Ks is that the earlier you start working on one, the better. The more money you save now, the more your money will have grown by the time you need to use it. It’s never too early to take steps toward paying your future self. Thanks to the power of potential compounding, saving early and for the entire length of your career can make a dramatic difference at retirement. One of the best ways to do so is through your workplace 401K plan, which offers important tax benefits and may come with matching funds from your employer and additionally, through and IRA plan.

6. How much should I contribute, and how often?

A generally accepted amount is 10 percent each pay period, however, you should invest as much as you feel you can afford if you want to maximize your retirement planning successfully. That being said, take into consideration other funds that require your financial attention: make sure you have enough in emergency funds and shorter-term savings, so that you don’t have to borrow or use any of your 401K money before you retire (see question 9). At the least, attempt to contribute as much as your employer matches, since that is a guaranteed return on the match, whether it’s 50 or 100 percent. Keep in mind that throughout the year, you have the option to adjust your contributions per pay period. So if you find yourself needing to play catch-up, you might decide to contribute up to 25 percent (depending on your salary—see the next question) for four months. Then, you can reduce your contribution to the minimum your employer match requires, depending on your financial situation.

7. What’s the maximum I can contribute?

There are annual limits to how much you can add to your 401K.

- For example in 2019, if you are under 50 years old, you can contribute a maximum of $19,000.

- If you’re 50 or older, you can make an additional catch-up contribution of as much as $6,000, for a total of up to $25,000.

Those limits change annually to track inflation.

8. What should I do with an old 401K?

You have a couple of options to weigh when leaving a company you’ve established a 401K with:

- Leave assets in your previous employer’s plan

- Move the assets into a rollover IRA or a Roth IRA

- Roll over the assets to a new employer’s workplace savings plan, if allowed

- Cash out or withdraw the funds

What you choose will depend on your current financial situation and your goals for your retirement plan. Be sure to evaluate the pros and cons of each option. Read more>>

9. How long do I need to wait before I can use my money?

Typically, you can’t withdraw any of your retirement money before age 59½ without incurring a 10 percent early withdrawal penalty from the IRS. This early distribution penalty is the cornerstone of the government’s campaign to discourage us from ravaging our savings before our golden years.

There are only two ways to dodge the penalty if you need to withdraw before you reach the age of 59½: If you’re at least 55 or do something called a Section 72(t) distribution. You can read more about it here on the IRS website

Whatever your age, your employer is required to give you a “Summary Plan Description” annually and upon request, which will address early retirement options in your 401K plan. If you rollover your 401K into an IRA, this option is not available to you.

The one other way around the 10 percent withdrawal penalty is through the “substantially equal periodic payment exception,” also known as a Section 72(t) distribution. This option generally gives you the least retirement pay-out available, and can be used by anyone with a 401K plan, regardless of age.

In a 72(t) withdrawal, the distributions must be “substantially equal” payments based upon your life expectancy. Once the distributions begin, they must continue for a period of five years or until you reach age 59½, whichever is longest.

You can read more about it here on the IRS website.

10. How many plans can I have?

There’s no legal limit to the number of 401Ks you can have at one time, but you can only contribute new money to the plan at your current employer. Therefore, it usually doesn’t make sense to keep open 401(k) plans from previous companies. To simplify things, better monitor your investments, and maintain control over your accounts, it’s a good idea to consolidate old 401Ks into your current 401K or an IRA.

Hopefully you’re now thinking about 401Ks more as 401(yay)s. And with this overview, you’ll be able to understand what they are and what they can do for your employees.

If you feel that you are not receiving adequate investment advice from your employer’s retirement plan provider, we can manage your 401K, TSA, TSP, Simple plan or pension plan. If your portfolio lost more than 10% in the last recession, you need to take another look at how you are managing risk. Research Financial Strategies can help. We will provide an unbiased review of your 401K and offer advice based on the best potential investment choices available in your 401K plan.

More reading:

Employer 401K Second Opinion

Rollovers of a 401K Retirement Plan

Planning For Retirement

What to do with an old 401K