It’s a pricey question.

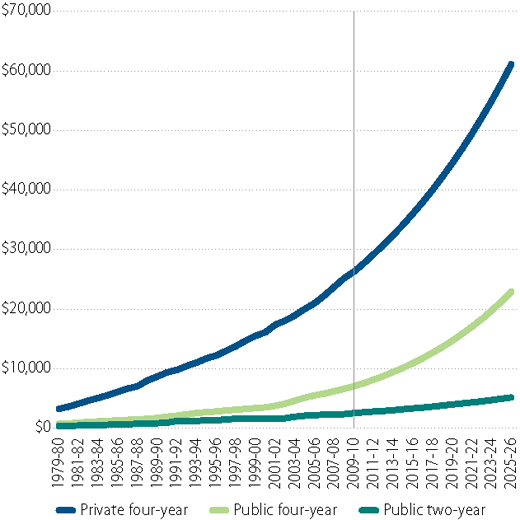

College Board estimated the average cost for full-time, in-state students who live on campus at four-year public colleges or universities during the 2017-18 school year is $25,290.1

Out-of-state students can expect to pay $40,940. Students who choose four-year, private, non-profit colleges and universities will spend about $50,900 a year.1

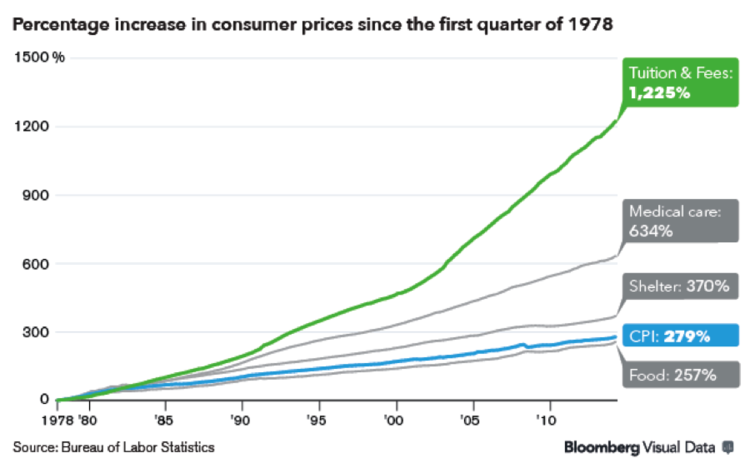

If pricing increases continue to follow the trend of the last five years, tuition and fees may increase by 3.2 percent a year without factoring in inflation.1, 2

The return on investment can be attractive

While the price tags attached are considerable, there is an argument to be made that the price of a college education is worth it.

Consider unemployment rates. The average unemployment rate in the United States in March 2018 was 3.6 percent, while the average unemployment rate for a person with a bachelor’s degree was 2.5 percent, reported the Bureau of Labor Statistics.3

A bachelor’s degree provides an income advantage, too.

The median (which is the mid-point, not the average) income for workers in the United States in March 2018 was $907 per week. The median income for Americans with high school diplomas was $712 per week. For people with bachelor’s degrees, median earnings were $1,173 per week, and for people with professional degrees, it was $1,836 per week.3

In other words, the $100,000 to $200,000 price tag attached to a bachelor’s degree could provide a lifetime income advantage of $1 million or more.*

There are alternatives to a four-year college

Of course, there is no guarantee a child will realize unemployment or income advantages, and college isn’t for everyone. When a child is not a passionate student, has little interest in additional schooling, or does not succeed in college, then skilled trades may be an option.

As the Baby Boom generation retires, a shortage of skilled workers has emerged, and it’s costing American businesses billions of dollars. Generally, skilled trades require fewer years of college or trade school and education alternatives – union and non-union apprenticeships, mentorships, or manufacturing-company training programs – may be available.4

Typically, skilled trade jobs pay well. Just think about the last time you wrote a check for plumbing, construction, or electrical work around your home. NPR reported, “In all, some 30 million jobs in the United States that pay an average of $55,000 per year don’t require bachelor’s degrees, according to the Georgetown Center on Education and the Workforce.”5

Sometimes, students with a passion for learning choose to pursue a dream rather than go to college. A variety of organizations, including the Thiel Foundation, provide support for select individuals. Thiel offers a two-year, $100,000 fellowship for students, ages 23 and younger, who forgo college and “build new things instead of sitting in a classroom.”6

Who should pay the bill?

This is a difficult question. The typical American family pays for college by combining scholarships and grants, personal income, savings, and loans, according to Sallie Mae’s 2017 How America Pays for College report. Income was derived from:7

- Scholarships and grants 35 percent

- Parents’ income and savings 23 percent

- Students’ loans 19 percent

- Students’ income and savings 11 percent

- Parents’ loans 8 percent

- Friends and relatives 4 percent

Not every family follows this formula. Often, the solution a particular family adopts is determined by its financial circumstances, values, and philosophy about raising children. Here are broad descriptions of three basic options for parents:

Not every family follows this formula. Often, the solution a particular family adopts is determined by its financial circumstances, values, and philosophy about raising children. Here are broad descriptions of three basic options for parents:

Parents pay all college costs. If you want to pay for college, you’ll need to start saving early and save for other financial goals at the same time. Sometimes, parents skimp on retirement savings to put more toward college. Many financial planners disagree with this choice because, as Time.com recently wrote, “…you and your child can borrow for college, while nobody lends for retirement.”8

529 College Savings Plans offer tax-advantages to parents and grandparents who are tucking money away for a child’s college costs.

Parents pay a portion of college costs. College cost sharing can be structured in a variety of ways. The variation chosen should suit the family. For instance, some parents may agree to pay tuition while children pay living expenses. Alternatively, parents may pay what they can afford from income and savings (without borrowing) and students are responsible for the remainder of the costs, even if students are required to borrow.

Another way to divide expenses is for parents to pay for undergraduate degrees, while children are responsible for graduate degrees. There are myriad variations on this theme.

Children pay all college costs. Some parents do not have the means to pay for college. Others believe in tough love or expect their children to ‘pull themselves up by their bootstraps.’9

No matter the reason, the student may benefit by declaring themselves financially independent from their parents, which may help them qualify for additional aid.

Sometimes, parents who require children to fund college pay off student loans as a graduation gift. As long as the amount is lower than the annual exclusion amount, gift taxes should not be triggered. Check with your tax advisor before taking any action.10

If you would like to discuss saving and paying for college or trade school, give us a call. We’re happy to talk with you.